The financial landscape is evolving rapidly, and central banks worldwide are embracing the concept of Central Bank Digital Currency (CBDC) as a means to modernize their monetary systems. CBDCs are digital currencies issued by central banks with their value linked to the issuing country’s official currency. The idea of CBDCs is gaining traction globally, with 87 countries actively exploring their implementation [1] . These 87 countries represent over 90 percent of global GDP. In this week's update we will delve deeper into how CBDCs will work, their benefits, and the unnerving risks they present to privacy and freedom. How Will CBDCs Work? In theory, CBDCs have the potential to digitize and replace physical currency. They are digital representations of a country's official currency, and will be issued and regulated by that country's central bank. The main goal for digitizing traditional money is to make it more accessible, efficient, and secure. The emergence of cryptocurrencies like Bitcoin and the growing importance of digital payments have propelled the exploration of CBDCs as a modern financial tool. CBDCs have the potential to revolutionize financial transactions by streamlining processes and reducing costs. In the current financial system, each bank operates its own payment tracking system, resulting in delays and inefficiencies when multiple banks are involved in a transaction [2] . However, since CBDCs would be handled by the central bank it would allow for all the transactions to be consolidated onto a single ledger, enabling instant clearing of payments and universal acceptance, regardless of the payment method or platform used [2] . Ultimately, if this idea comes to fruition, it will eliminate the need for banks that are not the central bank. Benefits of CBDCs CBDCs would require a complete overhaul of the financial system. Therefore, CBDCs must offer several significant advantages to justify that type of overhaul. Here are the some of the most prominent benefits for CBDCs: Reduced Costs - One key benefit is the potential for reduced costs. By shifting focus from physical infrastructure to digital finance, financial-service providers could save an estimated $400 billion annually in direct costs [3] . Increase speed - CBDCs have the capacity to enhance the speed and efficiency of electronic payment systems, benefiting both individuals and businesses. Appeal to the unbanked - CBDCs offer a solution for people who do not have access to a bank account. According to a survey from 2016, 1.6 billion people around the world did not have a bank account. Another statistic shows that less than 5% of adults do not have a bank account [3] . CBDCs have the potential to increase financial inclusion, empowering those without bank accounts, but adoption isn’t a guarantee as many underbanked people may favor the total anonymity that comes with using cash. Heightened Security - This is a byproduct of the speed and single bank ledger. Private key cryptography could be implemented for users to "sign off" on transactions digitally, and they would become finalized and unalterable in a short period of time [3] . Risks and Concerns While CBDCs offer numerous benefits, they also come with risks and concerns that must be carefully addressed. One major concern is the potential for increased governmental control. Although no central bank currently plans to restrict CBDC usage, the hypothetical possibility of the government deciding which purchases are permissible raises privacy and individual freedom concerns. Additionally, the traceability of digital currency may lead to increased taxation, as every transaction becomes easily traceable. Technological stability is another challenge, as evidenced by the temporary shutdown of the digital version of Eastern Caribbean DCash due to technical issues [4] . Let's take a moment to go more in depth on the potential for governmental control. The following is a quote from professor Eswar Prasad. Prasad is a professor at Cornell University and the author of The Future of Money: How the Digital Revolution Is Transforming Currencies and Finance. Prasad made this statement while speaking at the World Economic Forum's annual meeting of the new champions. “You could have, as I argue in my book, potentially better and some people might see a darker world, where the government decides that unit, so central bank money can be used to purchase some things but not other things that are deemed less desirable, like, say, ammunition or drugs or pornography or something of the sort. And that is very powerful in terms of the use of a CBDC and I think also extremely dangerous for central banks” [5] Prasad noted that he was only speaking hypothetically and said, “No central bank is contemplating any such uses for its CBDC but, as an academic, it is important for me to point out all the possibilities and potential—both good and bad—of a world in which all payments are digital and anonymity might be limited (relative to the use of cash).” [5] This is possible because CBDCs are programmable. For example, a CBDC could be programmable where it can only be used for certain items or even have an expiration date – which would ultimately force spending. This allows for CBDCs to make it much easier for a centralized authority to dictate and control human behavior because they can restrict the flow and opportunities if you are not behaving in a manner that they're requesting. This is very evident in China's social credit system. Use Cases for CBDCs It's important to balance the potential benefits of CBDCs with concerns related to individual privacy and governmental control. This is highlighted by China's social credit system. The China social credit system is a broad regulatory framework intended to report on the ‘trustworthiness’ of individuals, corporations, and governmental entities across China [6] . China’s “Social Credit System” rates its citizens based on their behaviors, and those who score well get privileges; those who score poorly do not. A citizen with a high score is likely to enjoy various privileges—high-speed internet, the ability to travel freely, access to the best restaurants, golf courses and nightclubs—that fellow citizens do not [7] . There are many ways to lose points and lower one’s social credit score, depending on the city where the offense takes place. Some of the more trivial score-lowering actions include: not visiting their parents on a frequent basis, jaywalking, walking a dog without putting it on a leash, smoking in a non-smoking zone, and cheating in online videogames [6] . A citizen with a poor social credit may experience one of these forms of punishment [6] : Travel bans Reports in 2019 indicated that 23 million people have been blacklisted from traveling by plane or train due to low social credit ratings maintained through China’s National Public Credit Information Center [6] . School bans The social credit score may prevent students from attending certain universities or schools if their parents have a poor social credit rating. For example, in 2018 a student was denied entry to University due to their father’s presence on a debtor blacklist [6] . Reduced employment prospects Employers will be able to consult blacklists when making their employment decisions. In addition, it is possible that some positions, such as government jobs, will be restricted to individuals who meet a certain social credit rating [6] . Increased scrutiny Businesses with poor scores may be subject to more audits or government inspections [6] . Public shaming In many cases, regulators have encouraged the ‘naming and shaming’ of individuals presented on blacklists. In addition, flow-on effects may make it difficult for businesses with low scores to build relationships with local partners who can be negatively impacted by their partnership [6] . CBDCs can also allow the government to be more targeted in their efforts to manage economic growth. One such case is the ability to combat inflation effectively. With the flexibility of CBDCs, central banks can implement different interest rates on specific balances or accounts, allowing for more precise monetary policy implementation. CBDCs also have the potential to support targeted stimulus efforts by directing funds to designated sectors or implementing expiration dates to encourage spending [8] . Implementation Timelines The timeline for CBDC implementation varies by country. In the United States, the Federal Reserve is already taking steps to address transaction inefficiencies by launching the FedNow digital payments system by the end of July 2023. This system aims to provide low-cost bill payments, money transfers, paychecks, government disbursements, and other consumer activities [9] . Time will tell when this will be fully implemented in the United States, but many see the implementation of FedNow as the first step toward a CBDC. Globally, a recent survey suggests that by 2030, approximately 24 central banks will have implemented digital currencies. This projection highlights the increasing global adoption and recognition of CBDCs as a fundamental part of future financial systems [10] . It is not a foregone conclusion that CBDCs will be implemented as there is plenty of opposition to the idea. Senator Cruz from Texas and Governor DeSantis from Florida have both introduced legislation to prohibit the Fed from establishing a CBDC [11][12] . If CBDCs take over the financial system, it appears there will be minimal options for those who do not want to participate in the system. Some of those options may include: using bitcoin that is established on a decentralized platform with options for privacy and anonymity, using physical precious metals like gold and silver, and/or exchanging value for value like in an archaic bartering system. Conclusion Central Bank Digital Currencies have the potential to revolutionize the way we transact and interact with financial systems. By leveraging digital technologies, CBDCs can offer reduced costs, increased speed, improved financial inclusion, and heightened security. However, careful consideration must be given to the risks associated with potential governmental control, privacy concerns, and technological stability. As countries progress toward a digital economy, CBDCs will play a pivotal role in shaping the future of money, transforming financial systems and enhancing economic efficiency on a global scale. The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situati on. Sources: https://www.mckinsey.com/featured-insights/mckinsey-explainers/what-is-central-bank-digital-currency-cbdc https://www.forbes.com/advisor/investing/digital-dollar/ https://www.mckinsey.com/featured-insights/mckinsey-explainers/what-is-central-bank-digital-currency-cbdc https://www.bloomberg.com/news/articles/2022-02-21/eastern-caribbean-dcash-outage-is-test-for-central-bank-digital-currencies?sref=YMVUXTCK https://apnews.com/article/fact-check-world-economic-forum-cashless-society-false-cbdc-592718364311 https://nhglobalpartners.com/china-social-credit-system-explained/ https://fee.org/articles/china-s-social-credit-system-sounds-pretty-dystopian-but-are-we-far-behind/ https://financialpost.com/fp-finance/cryptocurrency/central-bank-digital-currency-inflation-fighters-best-friend https://www.forbes.com/advisor/investing/digital-dollar/ https://www.reuters.com/markets/currencies/twenty-four-central-banks-will-have-digital-currencies-by-2030-bis-survey-2023-07-10/ https://www.cruz.senate.gov/newsroom/press-releases/sen-cruz-introduces-legislation-to-prohibit-the-fed-from-establishing-a-central-bank-digital-currency https://www.flgov.com/2023/03/20/governor-ron-desantis-announces-legislation-to-protect-floridians-from-a-federally-controlled-central-bank-digital-currency-and-surveillance-state/

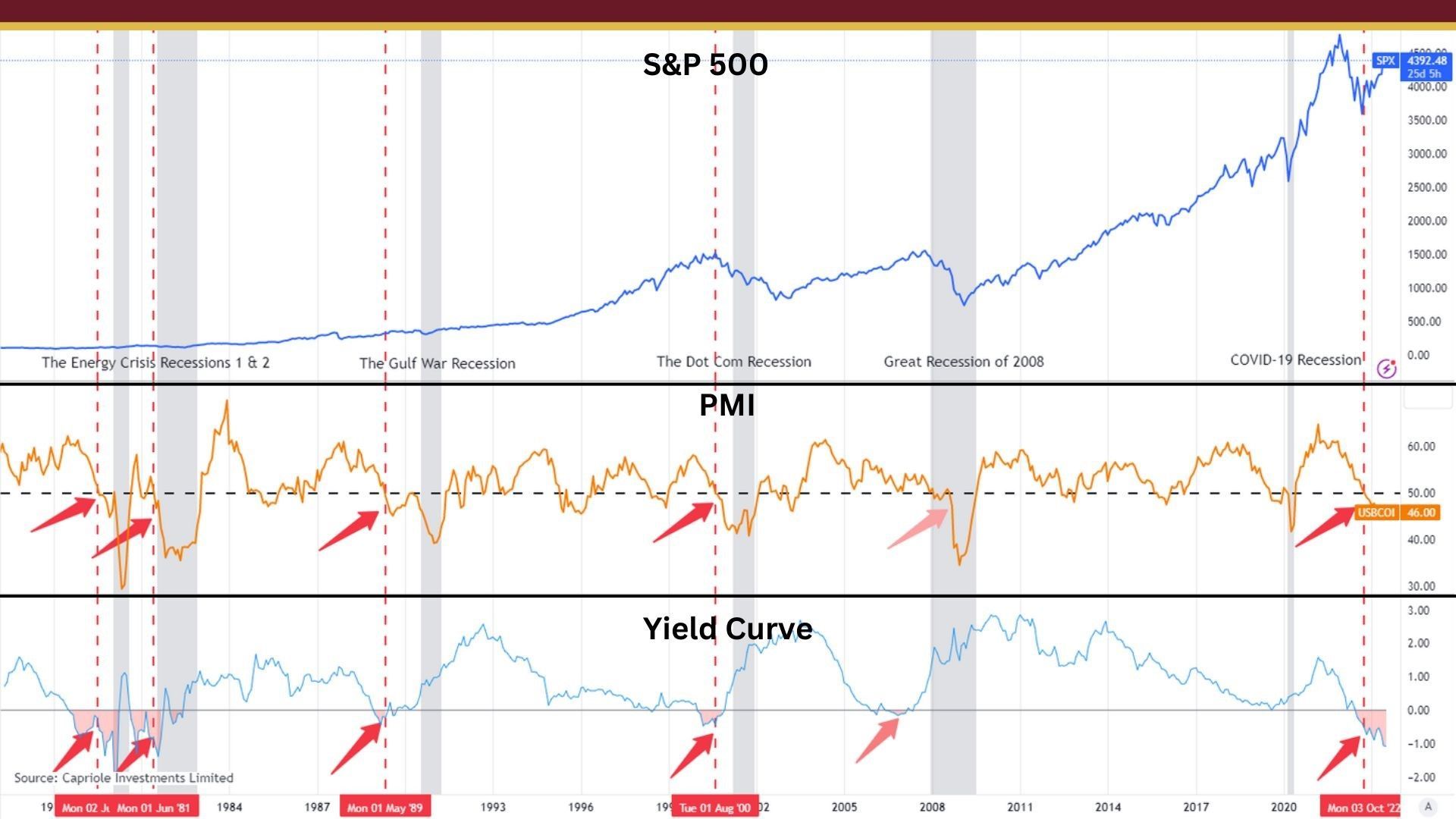

The global economy is facing increasing pressures, and there are growing concerns about a potential recession on the horizon. Two significant indicators that have historically foreshadowed economic downturns are an inverted yield curve and Purchasing Managers' Index (PMI) readings below 50. Over the past couple of months these two indicators have continued to point in the direction of an impending recession. In this week’s update, we will explore the historical context and significance of these indicators and analyze their current implications for the economy. Understanding the Inverted Yield Curve: An inverted yield curve occurs when short-term interest rates exceed long-term rates, typically reflected in the inversion of the two-year and 10-year Treasury yields. An inverted yield curve is often viewed as an indicator of a troubled economy because it deviates from the normal yield curve shape, where longer-term interest rates are typically higher than shorter-term rates. In an inverted yield curve scenario, short-term interest rates exceed long-term rates, implying that investors have lower expectations for future economic growth and inflation. This phenomenon has been a reliable recession predictor in the past, and suggests that the global economy is headed toward a recession despite the stock market trading near all-time highs 1 . The Fed chose to pause rate hikes during their June meeting, but many expect the rate hikes to continue in the future 2 . Persistently raising short-term rates in an inverted yield curve environment can increase the risk of an economic slowdown or recession. The inversion of the yield curve itself is often seen as a reliable predictor of economic downturns. By continuing to tighten monetary policy in this scenario, the Fed may unintentionally contribute to a deeper and more prolonged recessionary environment. PMIs Indicating Economic Contraction: PMIs, or Purchasing Managers' Indexes, are widely used economic indicators that provide valuable insights into the health and performance of various sectors within an economy. They are based on surveys conducted among purchasing managers in manufacturing, services, construction, or other sectors. The purpose of PMIs is to gauge the prevailing business conditions, sentiment, and trends within a specific sector or the overall economy. When a PMI reading falls below 50, it indicates economic contraction. The US manufacturing sector's recent contraction, raises concerns about the overall economic health and suggests a challenging road ahead 3 . The ISM Manufacturing PMI came in at 46 in June, down from 46.9 in May. This is the lowest reading since July 2020 3 . The manufacturing sector is followed closely due to it strong linkages with other sectors of the economy. Changes in manufacturing activity can impact supply chains, employment levels, and the performance of related industries. Manufacturing job losses can have a cascading effect on the economy, impacting consumer spending and business investment, and further contributing to the likelihood of a recession. Analysis of Current Economic Indicators:

Amidst upwardly revised GDP growth and declining jobless claims, underlying risks such as banks prioritizing financial stability and a decline in global manufacturing cast a shadow of uncertainty. In this week's update, we delve into crucial economic factors that are currently shaping the global landscape. By examining manufacturing PMI, banks' defensive stance, and the resilience observed in the US economy, we aim to provide valuable insights into the current state of affairs. Manufacturing PMI and Recession Signals The S&P Global Flash US Manufacturing PMI™ is a widely recognized economic indicator that measures the performance of the manufacturing sector. In June 2023, the PMI dropped to 46.9 [1] , raising concerns about a potential recession. The PMI measures the performance of the manufacturing sector based on surveys conducted among purchasing managers. It provides an overview of various aspects, including new orders, production levels, employment, supplier deliveries, and inventories. A reading above 50 indicates expansion, while a reading below 50 suggests contraction. This decline from 51.0 in May marks the lowest reading since February 2020. The contraction in the manufacturing sector is primarily driven by a slowdown in new orders and production [1] . Manufacturing PMI is an important indicator as it reflects the overall economic health of a country. The slowdown in new orders and production can be influenced by various factors such as changes in consumer demand, supply chain disruptions, labor shortages, trade policies, and global economic conditions. However, in this instance, the largest contributors are a drop in consumer demand and global economic conditions. Historically, there is a correlation between manufacturing PMI contractions and economic recessions. For instance, during the global financial crisis of 2008-2009, the PMI readings dropped significantly, signaling an economic downturn. Similarly, the PMI contraction in 2020 preceded the economic recession triggered by the COVID-19 pandemic. This makes it an important signal for investors and businesses to monitor [1] . Defensive Posture of Banks Worldwide Banks worldwide have been adopting a defensive posture, which further signals potential trouble ahead [2] . A defensive posture means that banks are taking measures to mitigate potential risks and ensure financial stability. Specific actions can include increasing capital reserves, tightening lending standards, reducing exposure to high-risk assets, enhancing risk management practices, and diversifying their portfolios to minimize vulnerabilities. The cautious approach of banks reflects their awareness of potential risks in the economy. By adopting a defensive posture, banks aim to protect themselves from financial shocks, economic downturns, and uncertainties. This cautious approach contributes to overall economic stability by reducing the likelihood of systemic risks and enhancing the resilience of the financial system. When banks take this defensive posture, it becomes a greater priority to be fiscally stable than make loans - which are the main revenue source for banks. In my opinion, this is something to watch as many commerical real estate loans come due in the next 12-18 months. As interest rates have significantly increased over the past 12 months, it will be challenging for businesses to renew those loans which will negatively impact the banks and their revenue [3] . Signs of Resilience in the US Economy Despite concerns highlighted by manufacturing PMI numbers and the defensive posture of banks, positive news emerges from the US economy. First-quarter GDP growth has been revised up to 2.0% from 1.3% [4] , indicating ongoing economic expansion. The revision of first-quarter GDP growth from 1.3% to 2.0% indicates that the US economy is expanding at a slightly faster pace than previously estimated. This upward revision suggests stronger economic performance and reflects positive momentum. Additionally, weekly jobless claims in the United States fell to their lowest level since October 2021 [4] . The decline in jobless claims to their lowest level since October 2021 signifies a that the labor market is showing signs of resilience. In previous weeks we've discussed the impact of labor hoarding and how it could be affecting these weekly numbers. The revised GDP growth and the decline in jobless claims reflect the resilience of the US economy. However, it is important to note that the economy is growing at a slower pace compared to previous quarters [4] . The Federal Reserve's efforts to combat inflation may influence future economic growth. While positive indicators exist, rising inflation and external factors such as the war in Ukraine could impact the possibility of a future recession [4] . Conclusion In summary, considering the manufacturing PMI numbers, the defensive stance of banks, and the positive indicators in the US economy, the outlook for the next 6-12 months remains uncertain as we are getting mixed signals across the global economy. There are some encouraging signs for the US economy as the labor market appears to be resilient. However, there's an undertone of vulnerability that warns of potential risks that could lead to a sharper downturn if not carefully managed. Our Directional Portfolios aim to build a portfolio that will adjust with the business cycle. If you'd like to learn more, you can call or text at 678.884.8841 or email us at connect@findabundance.com . The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situati on. Sources: https://www.pmi.spglobal.com/Public/Home/PressRelease/6e8efbfbddde43f29eb12c5193939625 https://www.ecb.europa.eu/press/key/date/2023/html/ecb.sp230302~41273ad467.en.html https://fortune.com/2023/06/26/commercial-real-estate-office-downturn-outlook-goldman-sachs-morgan-stanley-ubs-pwc-bofa/ https://www.reuters.com/markets/us/us-weekly-jobless-claims-fall-first-quarter-gdp-revised-higher-2023-06-29/

Introduction The global economy is showing worrisome signs of a synchronized deflationary recession, with China's recent interest rate cut serving as a significant indicator. However, central banks worldwide remain focused on inflation and tight labor markets, overlooking the potential risks associated with increasing rates during an economic slowdown. In this week's article, we will explore the implications of these trends and highlight the importance of a comprehensive approach to address the challenges ahead. Overview of Recent Rate Cuts in China China's decision to cut lending benchmarks comes as authorities seek to revitalize a slowing economic recovery. The one-year loan prime rate (LPR) was lowered by 0.1 percent to 3.55%, while the five-year LPR was reduced by the same margin to 4.20% [1] . Although the cuts were anticipated, the smaller-than-expected reduction in the five-year rate disappointed some investors, leading to a drop in the Hang Seng Mainland Properties Index and a dip in broader Asian stock markets. These rate cuts aim to lower the cost of new loans and ease interest payments on existing loans [1 . While they are expected to offer modest support to economic activity, weak credit demand may prevent a sharp acceleration in credit growth. As one of the world's largest economies, China's actions often foreshadow wider economic shifts. In my opinion, this rate cut serves as a cautionary signal that should not be ignored in assessing the current economic landscape. Divergent Monetary Policy Worldwide The global landscape of monetary policy reveals a divergence in approaches among major central banks. Central banks typically prioritize inflation as a key economic indicator, while the labor market's tightness also plays a crucial role [2] . However, an exclusive focus on inflation may lead to an incomplete understanding of the overall economic health. Neglecting signs of an economic slowdown, such as a tight labor market, can hinder effective policymaking and response strategies. The European Central Bank (ECB) recently hiked rates and signaled a worsening inflation outlook. In contrast, the Federal Reserve opted to pause rate hikes during their most recent meeting but have suggested future rate hikes later this year. These central banks are creating a hyper focus on inflation because they believe that the labor markets are in good shape as unemployment numbers have stayed a good level. Yet, according to a Skynova survey in February, 91% of businesses are actively labor hoarding [3] . Labor hoarding is where businesses retain a larger workforce than necessary [3] . The rationale behind this practice lies in the long-term cost-benefit analysis and the desire to maintain a positive outlook for the firm. I believe this is happening because many business owners expect a shallow recession. Therefore, it's more cost effective to hold on to labor and make it through a shallow recession than it is to lay off and rehire a large amount of your workforce. However, if the China rate cuts are signaling a greater economic slowdown, businesses will be forced to lay off the excess labor they have been retaining, magnifying the impact of the recession. Global Implications of China's Rate Cuts China's rate cuts hold significant implications for the global economy. As the second-largest economy in the world, China's actions have a ripple effect on global trade, investment, and financial markets. The rate cuts are expected to reduce loan costs and provide some support to economic activity, which could have positive effects on global trade dynamics. We'll see if China's rate cuts could influence the decisions of other major central banks. The Federal Reserve, for example, may consider the global economic environment and China's actions when determining its future rate hike plans. The ECB, which recently hiked rates and expressed the likelihood of further increases, may also be influenced by China's monetary policy decisions. These interconnected relationships emphasize the importance of monitoring China's actions and their potential implications for global monetary policy coordination. Conclusion As the world's second-largest economy, China's monetary policy decisions carry significant weight that should not be overlooked. While the rate cuts are expected to provide support to economic activity in China, their impact on the global stage is also of great importance. In general, rate cuts signal that an economy needs to be stimulated due to a lack of demand. I believe we're already seeing signs of a globally synchronized recession as Germany technically entered a recession in May [4] and New Zealand technically fell into a recession in the past couple of weeks [5] . Our Directional Portfolios aim to build a portfolio that will adjust with the business cycle. If you'd like to learn more, you can call or text at 678.884.8841 or email us at connect@findabundance.com . The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situati on. Sources: https://www.reuters.com/world/china/china-cuts-lending-benchmarks-first-time-10-months-support-economy-2023-06-20/ https://www.cnbc.com/2023/06/19/fed-ecb-boj-pboc-central-banks-monetary-policy-decision-are-diverging.html https://www.realclearmarkets.com/articles/2023/06/16/policymakers_will_need_a_miracle_not_a_pause_941110.html https://www.conference-board.org/blog/global-economy/Germany-GDP-forecast-recession https://www.bbc.com/news/business-65911732

In the past week the stock market has technically entered a new bull market. Bull and bear markets are technically defined by a 20% move from the recent low. We recently saw the S&P cross this threshold as it surged 20% since the lows in October 2022 [1] . In the world of investing, the emergence of a new bull market is often met with excitement and optimism. However, the current situation is marked by an intriguing contradiction—the markets have technically entered a new bull market while the broader economy shows signs of a slowdown. In this week’s update, we will explore this paradox, examining the indicators of a new bull market while considering the challenges posed by a sluggish economy. Market Resurgence: A Technical New Bull Market Despite the economic headwinds, numerous experts argue that the markets have entered a new bull market. There is a lot of enthusiasm around the market gains and the newly declared bull market. Yet, it's important to realize that the market is not always a good judge of the economy. In fact, it's a better measure on how people feel about where the market is heading. A positive move in the market is suggesting a positive outlook. One way to determine this sentiment is to follow CNN's Fear and Greed Index. The Fear & Greed Index is a way to gauge stock market movements and whether stocks are fairly priced. The theory is based on the logic that excessive fear tends to drive down share prices, and too much greed tends to have the opposite effect [2] . The index has a rating of 0-100, and we're currently sitting at a level of 82 which is categorized as "extreme greed" [3] . What does this mean for the future of the markets? I don't know … time will tell, but there are a definitely a handful of signs that point to a slowing economy that could quickly shift the renewed optimism back to pessimism. Economic Concerns: Signs of a Slowing Economy Amidst the market's resurgence, it's essential to acknowledge the concerning state of the economy. US manufacturing is experiencing minimal growth, while inventories have reached levels that hinder future expansion [4] . Additionally, the labor market, although the numbers have stayed strong, exhibits signs of strain. In my opinion, the data is suggesting that demand is slowing and it's forcing businesses into making difficult financial decisions. Essentially, cutting labor force is the last and final option to reduce costs. Things have stayed very stable but we're starting to see initial claims of unemployment continue to tick up each week [5] . We're also seeing companies resort to labor hoarding [6] and reducing hours worked [7] to retain employees. Labor hoarding is a sign that businesses are worried about the future and are trying to protect themselves from a potential recession. There are a number of reasons why businesses are hoarding labor. One reason is that the labor market is very tight, with unemployment at a record low. This makes it difficult for businesses to find qualified workers, and businesses are reluctant to lay off workers who they may need in the future. [6] Another reason for labor hoarding is that businesses are worried about a potential recession. If a recession does occur, businesses may need to reduce production or even close down. By hoarding labor, businesses can ensure that they have the staff they need to weather a recession. [6] The Lingering Banking Crisis The other major red flag for me are the signs of the lingering banking crisis. This is not something that has stayed in the headlines. In fact, I believe part of the optimism in the current markets is due to the fact that many believed the banking crisis that occurred earlier this year would have a major impact on the labor markets. Therefore, it makes sense why optimism would return when the crisis seems to have passed with little impact to the labor markets. Despite outward signs of recovery, it does not appear that banks have returned to their normal lending activities. This is highlighted by the idea that a well known real estate developer in Texas is having a difficult time finding a bank willing to lend to them for their projects [8] . Despite a demand for new apartments, Howard Hughes Corp., a real estate developer backed by hedge fund manager Bill Ackman, is struggling to find financing for new apartment projects. The company has reached out to dozens of lenders, but none have shown interest in providing funding. This is due to a number of factors, including rising interest rates and concerns about the overall health of the real estate market. As a result, Howard Hughes is having to delay or cancel some of its planned projects. [8] This is a sign of the challenges facing the real estate industry, as lenders become more cautious about lending money for new projects. This is also a sign that banks are not back to business as usual because lending is the life blood of their business model. This can be signaling that banks are not confident about the future and doing everything they can to avoid risk and potential default. Conclusion: To comprehend this paradox, it is crucial to consider the interplay between market sentiment and economic indicators. While economic indicators reflect the current state of affairs, market sentiment often guides investor behavior. The surge in the market, despite a sluggish economy, underscores the influence of sentiment over economic realities. Solely relying on economic indicators may not capture the complexities of the market. This presents investors with a unique challenge—managing a new bull market amidst a slowing economy. While the markets display renewed vigor, economic indicators warn of potential hurdles. To navigate this paradox, a balanced approach is crucial and we must remain attentive to both market sentiment and economic realities. Our Directional Portfolios aim to build a portfolio that will adjust with the business cycle. If you'd like to learn more, you can call or text at 678.884.8841 or email us at connect@findabundance.com . The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situati on. Sources: https://www.nasdaq.com/articles/a-new-bull-market-has-begun https://www.cnn.com/markets/fear-and-greed?utm_source=business_ribbon#fng-faq https://www.cnn.com/markets/fear-and-greed?utm_source=business_ribbon https://www.reuters.com/markets/us/us-manufacturing-output-barely-grows-may-2023-06-15/ https://apnews.com/article/unemployment-benefits-jobless-claims-layoffs-labor-140978ffe6a95f5a4efa84406d5e9421 https://www.cnn.com/2023/06/08/economy/labor-hoarding-economy/index.html https://fred.stlouisfed.org/series/AWHAETP https://www.bloomberg.com/news/articles/2023-06-08/real-estate-builder-backed-by-ackman-says-lenders-rejecting-new-apartment-deals#xj4y7vzkg

The soft landing narrative is on its last leg. In economics, a soft landing refers to a smooth transition from a period of rapid growth to a more sustainable level. Many experts had hoped that the global economy would experience a soft landing, supported by three main arguments. However, as we delve deeper into the current economic landscape, it becomes apparent that these arguments are not playing out as expected. This week's article aims to explore the reasons behind the diminishing likelihood of a soft landing, with a specific focus on the faltering arguments surrounding China's reopening, Europe's struggle to rebound, and the deteriorating US job market. China's Reopening: A Disappointing Boost to the Economy One of the key arguments put forth for a soft landing was the expectation that China's reopening would stimulate global economic growth. However, recent developments indicate that China's reopening is not proceeding as anticipated. The economic data reported for China in the month of May shows declining trade and an economic slowdown. The country's trade volumes have decreased, resulting in a contraction in exports and reduced consumer spending. According to the report, China shows a 7.5% decline in exports from last May and a 4.5% decline in imports [1] . April’s “disappointing activity data” suggests “China’s domestic demand recovery has lost steam following the reopening-induced bounce,” Said Lloyd Chan of Oxford Economics [1] . These factors have hindered the expected economic boost, highlighting the challenges faced by China and its potential impact on the global economy. Europe's Struggle: Failing to Rebound After Energy Crisis Another argument for a soft landing revolved around the belief that Europe would rebound following the energy crisis that ended around March of this year [2] . However, there continues to be a slowing of global economies, with a particular emphasis on Germany. German factory orders, a significant indicator for Europe's largest economy, have dipped, indicating a disappointing start to the second quarter. Furthermore, Germany experienced a contraction in its gross domestic product (GDP) during the first quarter of the year, marking a potential recession [3] . Germany is traditionally one of the strongest economies in Europe. These developments raise concerns about Europe's economic recovery and its ability to rebound as initially anticipated. In addition to what we're seeing in Germany, there is supporting evidence that economic slowdowns are happening across the world. A World Bank report estimates that the international economy will expand just 2.1% in 2023 after growing 3.1% in 2022 [4] . Indermit Gill, the World Bank’s chief economist, called the latest findings “another gloomy report." The bank, he said, expects “last year’s sharp and synchronized slowdown to continue to this year into a sharp slowdown.” [4] US Job Market: Struggling Amid Rising Jobless Claims The final argument being made for the soft landing was a strong jobs market. For the most part the US job market remains strong but is beginning to face some challenges. As of this past week, jobless claims in the US are at their highest levels since 2021 [5] . This rise in jobless claims signifies a weakening job market, with economic uncertainty and reduced business activity as contributing factors. The struggling job market in the US has significant implications for the overall health of the economy and casts doubt on the likelihood of a soft landing. The job market serves as a crucial indicator of economic stability and consumer confidence, making this downturn a cause for concern. Conclusion As we analyze the current state of the global economy, it becomes evident that the arguments supporting a soft landing are losing traction. China's reopening has not generated the expected economic boost, with declining trade and reduced consumer spending dampening its impact. Europe, specifically Germany, is facing economic challenges, as seen in the slowing factory orders and the potential onset of a recession. The US job market is also struggling, as evidenced by the increase in jobless claims. These factors collectively question the feasibility of a soft landing in the global economy. In conclusion, while hopes were high for a soft landing, the reality is painting a different picture. The arguments surrounding China's reopening, Europe's rebound, and the strength of the US job market are not playing out as anticipated. By acknowledging these challenges and adapting our strategies, we can better navigate the evolving economic landscape and work towards achieving a sustainable and resilient global economy. Our Directional Portfolios aim to build a portfolio that will adjust with the business cycle. If you'd like to learn more, you can call or text at 678.884.8841 or email us at connect@findabundance.com . The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situati on. Sources: [1]: https://apnews.com/article/china-trade-economy-recovery-f56dc3c1b60446d55560be4aff9eb1d8 [2]: https://www.politico.eu/article/europe-is-out-of-the-immediate-energy-crisis/ [3]: https://apnews.com/article/germany-industrial-orders-economy-7210f9ec27d632d99b033dca2bb8e15e [4]: https://abcnews.go.com/US/wireStory/world-bank-offers-dim-outlook-global-economy-face-99867179 [5]: https://www.nasdaq.com/articles/us-weekly-jobless-claims-jump-to-1-1-2-year-high

In a time of significant challenges, the United States is currently facing two critical issues: the debt ceiling debate and the state of the job market. The consequences of inaction in these areas can have far-reaching impacts on the economy, financial markets, and individual livelihoods. In this article, we will delve into the potential consequences of inaction, proposed amendments, the resilience of the job market, and the implications for financial markets. It is vital to address these challenges promptly and thoughtfully to ensure economic stability and maintain investor confidence. Understanding the Debt Ceiling and Consequences of Inaction Having discussed the debt ceiling in previous weeks we will not dive deep into the ramifications of potential default as we know failure to pass the debt ceiling bill by the June 5 deadline could result in an inability to meet financial obligations, including debt payments, Social Security benefits, and military salaries. This scenario would trigger a severe financial crisis, impacting not only the government but also businesses and individuals. The uncertainty surrounding a potential default would most likely lead to market volatility and a loss of investor confidence. Lawmakers have proposed amendments to the debt ceiling bill, aiming to introduce spending cuts and increase defense spending [1] . However, any changes to the bill would require it to be sent back to the House for review, potentially causing delays and creating additional uncertainty. It is essential for lawmakers to find common ground, foster bipartisan cooperation, and consider alternative solutions that can ensure the timely passage of the debt ceiling bill. A swift resolution to this debate is critical to instill market stability and investor trust. Job Market Resilience, Challenges, and Industry Impact This past week the Federal reserve published one of their Beige Book reports. It provides a qualitative assessment of the current economic conditions in each of the 12 Federal Reserve districts across the United States. The report gathers information from various sources, including businesses, economists, market experts, and other contacts within each district. In addition to their report, we've seen a recent uptick in unemployment claims and layoffs in May. In spite of a recent increase in Americans filing for unemployment benefits, the job market has shown resilience. Employers, faced with challenges in finding qualified employees, have generally held onto their workforce. However, certain industries, such as technology and interest rate-sensitive sectors, have experienced job cuts due to economic uncertainties. These challenges highlight the need for measures and initiatives to address industry-specific issues and foster a sustainable job market recovery. Economists predict a slowdown in job growth, but there are hopes that the unemployment rate is will rise only slightly [2] . The Federal Reserve's Beige Book report describes the job market as strong, but it also highlights that some businesses are pausing hiring or reducing their workforce due to weaker demand or economic uncertainties. This cautious approach may impact consumer spending and overall economic growth. Furthermore, a default or prolonged debate on the debt ceiling could have long-term implications for the economy, including higher borrowing costs, reduced business investment, and diminished consumer confidence. Navigating the Challenges and Ensuring Economic Stability At the time of this writing, the debt ceiling bill has been approved in the House and passed to the Senate for the final stamp of approval [1] . The debt ceiling debate and the state of the job market have significant implications for financial markets. Uncertainty surrounding the debt ceiling can lead to increased market volatility, as investors become cautious about the government's ability to meet its financial obligations. Investors will closely monitor the progress of the debt ceiling bill, and any signs of prolonged debate or a potential default can impact market sentiment. Therefore, a timely resolution to the debt ceiling debate is crucial for restoring and maintaining investor confidence. Conclusion: The outcome of the debt ceiling debate and the state of the job market have significant implications for financial markets. Investor confidence is closely tied to the government's ability to manage its financial obligations and maintain economic stability. Any signs of prolonged debate or a potential default can lead to increased market volatility and a loss of investor trust. Therefore, a swift resolution to the debt ceiling issue is crucial for restoring and maintaining market stability. Furthermore, the long-term implications of these challenges should not be overlooked. A default or prolonged debate could result in higher borrowing costs, reduced business investment, and diminished consumer confidence. This can hamper economic growth and have far-reaching consequences across various sectors. Policymakers must consider the potential ripple effects and work towards mitigating risks to ensure a sustainable and inclusive recovery. In conclusion, the debt ceiling debate and the state of the job market pose critical challenges for the United States. Swift action is necessary to pass the debt ceiling bill, avoid a potential default, and maintain investor confidence. The resilience of the job market is commendable, but efforts should be made to address industry-specific issues and foster a sustainable recovery. By prioritizing economic stability, finding common ground, and investing in initiatives that support growth and innovation, we can navigate these challenges and build a stronger and more inclusive economy for the future. The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situati on . Sources: https://abcnews.go.com/Politics/debt-ceiling-drama-shifts-senate-expect/story?id=99735146 https://finance.yahoo.com/news/u-weekly-jobless-claims-rise-124208133.html

The markets have started to increasingly feel uncertain without a clear resolution coming for the debt ceiling. Failing to come to a timely decision raising concerns about the possibility of an unprecedented US debt default. The potential consequences of such a scenario would have far-reaching implications for everyday Americans. In this article, we will delve into the possible effects of a US debt default on the lives of ordinary citizens and the ripple effects that will take place in the markets. The US debt ceiling, also known as the debt limit, is a statutory limit on the total amount of debt that the US government can legally borrow. It represents the maximum level of debt the government can accumulate to fund its operations and meet its financial obligations. The US financial system is often referred to as a debt-based system because it relies heavily on borrowing and lending activities to fuel economic growth and facilitate various transactions. Without coming to a new arrangement, the government would not be able to keep funding their operations as they are today. The factors that could potentially lead to a US debt default range from political gridlock and excessive spending to a global economic crisis. Immediate Impact on Financial Markets A US debt default would trigger a wave of uncertainty in financial markets. Stock markets would experience heightened volatility, causing disruptions for investors and potentially eroding retirement savings. For example, during the 2011 debt ceiling debate the S&P 500 declined close to 15%. [1] A default would also most likely result in a downgrade for the US credit rating. A downgrade in rating would cause borrowing costs to skyrocket and affect mortgages, loans, and credit card interest rates. Moreover, the US dollar may face devaluation, reducing Americans' purchasing power and raising the cost of imported goods. Job Market and Employment The economic contraction resulting from a debt default would have adverse effects on businesses. Naturally the demand for goods and services would fall as everyone would be seeking to save their money and avoid large losses from the stock market. A decline in demand would negatively impact revenue and sales which will ultimately lead to job losses and increased unemployment rates. Finding new employment opportunities would become increasingly challenging as companies struggle to stay afloat amidst the economic turmoil. The ripple effect of reduced consumer spending would exacerbate the job market's instability. Government Services and Social Programs A debt default would force the government to implement significant budget cuts to reduce spending. Essential services such as healthcare, education, and infrastructure maintenance could face severe funding reductions, negatively impacting Americans' quality of life. Additionally, social programs like Social Security and Medicare may face uncertainty, leaving retirees and vulnerable populations in a state of financial insecurity. This would have a severe impact on the income of many retirees. According to the National Committee to Preserve Social Security and Medicare, social security payments are responsible for 50% of the household income for two-thirds of those who receive social security, and for 40% of recipients their social security benefits consist of 90% of their income [2] . Higher Cost of Living Economic instability resulting from a debt default often leads to inflationary pressures. As the value of the dollar declines, the cost of goods and services tends to rise. Everyday Americans would face the burden of a higher cost of living, affecting their household budgets and diminishing their disposable income. Basic necessities such as food, utilities, and transportation would become more expensive, and magnify the financial strain that many people have been feeling for the past year. International Reputation and Trade A US debt default would erode the trust and credibility of the United States in global financial markets. Foreign investors may hesitate to invest in the US economy, leading to reduced foreign direct investment and limited access to capital. The decline in international trade would further impede economic growth, potentially causing long-term damage to the US economy. Conclusion The potential consequences of a US debt default are far-reaching and would significantly impact everyday Americans. From the immediate effects on financial markets and increased borrowing costs to job losses, reduced government services, and higher living expenses, the ramifications would be felt across various aspects of life. In my opinion, because of all these ramifications, a default is unlikely. I anticipate a decision to be made before the anticipated date of June 1st, but also anticipate increased market volatility while we wait for a decision. Our Directional Portfolios aim to build a portfolio that will adjust with the business cycle. If you'd like to learn more, you can call or text at 678.884.8841 or email us at connect@findabundance.com . The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situati on . End Notes: https://www.americanprogress.org/article/default-would-have-a-catastrophic-impact-on-the-economy/ https://www.cnn.com/2023/05/24/politics/social-security-debt-ceiling/index.html

The global economic landscape is constantly evolving, influenced by various factors and events. In the wake of global economic struggles, China's reopening was hailed as a beacon of hope for the world economy. However, as reality unfolds, it has become evident that the anticipated economic boom has encountered unexpected obstacles. China's slowing industrial profit and factory output, coupled with shifting consumer spending habits and an impending decline in commercial real estate, paint a somber picture. This article delves into the intricacies of these interconnected factors, shedding light on the uncertain path ahead. Join us as we navigate the shadows cast by China's reopening, evolving consumer behavior, and the precipice of a global economic decline. China's Reopening: A Different Reality China's reopening after a second round of COVID-19 lockdowns is not unfolding as the rest of the world would've hoped [1] . At the beginning of the year, China reopened its borders after three years of COVID closures. Initially, optimism surrounded China's reopening as it could kick-start economies across the world, but recent data on industrial profit and factory output suggest a different reality [1] . China's economic momentum seems to be slowing down, with concerns over slack post-COVID economic growth [2] . China's economic data for April fell well below expectations. They only saw a 5.9% increase in industrial production when they expected close to 11% growth, and retail sales grew by 18% when many economists anticipated growth around 21% [1] . The impact of China's economic performance extends beyond its borders, affecting global markets and trade dynamics. Here are a few reasons why China's economy is important to the rest of the world: Size and Growth: China is the world's second-largest economy behind the United States. Its sheer size makes it a major player in global economic affairs. Over the past few decades, China has experienced rapid economic growth, lifting hundreds of millions of people out of poverty and creating a burgeoning middle class. The expansion of China's economy has had a profound impact on global trade and investment flows. Consumption and Demand: As China's middle class continues to grow, so does its consumer market. Chinese consumers have become increasingly important drivers of global demand for goods and services. Many multinational companies consider China as a crucial market for their products and services, and the preferences and purchasing power of Chinese consumers have a significant influence on global industries such as automotive, luxury goods, technology, and more. Investment and Capital Flows: China attracts substantial foreign investment, both in terms of direct investment and portfolio investment. Foreign companies seek opportunities to access China's large market, establish production facilities, or partner with Chinese firms. Moreover, China has actively invested in foreign assets, including infrastructure projects in developing countries, which can impact regional and global economic dynamics. Therefore, a reopening of their economy would help initiate the flow of money across global markets. Yet, if demand wanes (like it appears to be) then these opportunities go away and will not provide the opportunities that many hoped. Global Economic Stability: Given its size and interconnectedness with the global economy, China's economic stability is crucial for overall global economic stability. Any significant disruptions in China's economy, such as a financial crisis or a severe slowdown, can have spillover effects on other countries through trade, financial, and confidence channels. In summary, changes in China's economy can reverberate globally, affecting businesses, industries, and countries around the world. Consumer Behavior Shift: Insights from Home Depot and Target Earnings The earnings reports of Home Depot and Target provide valuable insights into changing consumer behavior [4][5] . Home Depot, reported it's first decline in earnings in over three years [4] . The decline in earnings is a sign that many consumers are becoming more cautious as they fear a recession. Home Depot saw a 6.6% decline in earnings per share from this time last year. Home Depot also revised their sales projections down by 2%-5% for the remainder of the year citing "continued uncertainty regarding consumer demand." [4] Target's earnings report also revealed consumers' altered spending habits as they're seeing consumers spend more on essential items instead of clothing [5] . They've also experienced losses incurred by a rise in shoplifting due to organized retail crime. They estimate that this trend may cost them $500 million in profitability this year [5] . These shoplifters are resorting to this type of crime as a way to make money because they will resell the stolen items online. Commercial Real Estate Challenges: A Looming Decline The commercial real estate sector is facing significant challenges, raising concerns about a potential decline. A rise in distressed sales has become a clear signal of the beleaguered state of the office market [6] . These large investors are getting rid of properties at fire sale prices. Here are a few transactions: Blackstone sold the Griffin Towers office complex in Santa Ana for $82 million, or about 36% less than the firm paid in 2014 [6] . Principal Financial Group sold a Parsippany, N.J., office building for $14.3 million, down from the $52 million it paid in 2008 [6] . The tower at 350 California in San Francisco, valued at $300 million in 2019, is expected to trade at about $60 million, or roughly 80% below that previous valuation [6] . Various factors contribute to this situation, including remote work trends, changing office space requirements, and economic uncertainty. In my opinion, these transactions may be foreshadowing a large decline in commerical real estate values, and if that's the case, these investors are willing to take large losses now in order to prevent greater losses in the future. If the commercial real estate sector experiences a substantial decline, it could have far-reaching consequences for investors, businesses, and the overall economy. Conclusion China's reopening, changing consumer spending habits as indicated by Home Depot and Target earnings, and the challenges faced by the commercial real estate sector all contribute to the evolving global economic landscape. They're continual signs that both consumers and businesses are feeling the financial pressure. Abundance is here to help you prosper regardless of what happens next in the economy. Our Directional Portfolios aim to build a portfolio that will adjust with the business cycle. If you'd like to learn more, you can call or text at 678.884.8841 or email us at connect@findabundance.com . The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation. Sources: [1] CNBC. (2023, May 16). China's industrial profit growth slows sharply in April. Retrieved from [ https://www.cnbc.com/2023/05/16/chinas-data-industrial-profit.html ] [2] Reuters. (2023, May 16). China's factory output, consumption highlight slack post-COVID economic momentum. Retrieved from [ https://www.reuters.com/world/china/chinas-factory-output-consumption-highlight-slack-post-covid-economic-momentum-2023-05-16/ ] [3] AP News. (2023, May 16). China exports boom but outlook gloomy as virus surges. Retrieved from [ https://apnews.com/article/china-economy-export-1c99e06f41260c5c56156fb5c0ea3626 ] [4] Investors.com. (n.d.). Home Depot Earnings Beat, Dow Jones Giant Raises Outlook. Retrieved from [ https://www.investors.com/news/home-depot-earnings-dow-jones-hd-stock/ ] [5] CNN Business. (2023, May 17). Target reports strong earnings as consumers shift spending habits. Retrieved from [ https://www.cnn.com/2023/05/17/business/target-earnings/index.html ] [6] The Wall Street Journal. (n.d.). https://www.wsj.com/articles/rise-in-distressed-sales-signals-new-chapter-for-beleaguered-office-market-bbff313c

Are we heading towards a deflationary economy? The recent decline in manufacturing orders, ongoing banking crises, and a drop in small business optimism all point towards potential future unemployment rates on the rise. A deflationary economy is when prices for things we buy go down instead of up. This might sound like a good thing, but it can actually be a problem because it can cause people to stop spending money. In this week’s article, we will analyze a few of the recent economic indicators that support the existence of a deflationary economy. The Decline of German Manufacturing: What Does It Mean for the Rest of Europe? First, let's take a look at the manufacturing sector in Germany. The manufacturing sector continued to perform poorly in April 2023, with the worst performance since May of 2020. [1] The factory sector has been contracting for ten consecutive months. This has put continued downward pressure on new orders due to customer hesitancy and efforts to unwind buffer stocks. Average purchase prices fell the most since December of 2019, and expectations ticked up to a 14-month high. [2] When the average purchasing price of is going down, it means that manufacturers are paying less for the raw materials and other inputs needed to produce their products. Lower purchasing prices may seem like a good thing for manufacturers, as it means they can reduce their costs and potentially improve their profit margins. However, if prices continue to fall and the overall economy enters a deflationary period, it can have negative effects on the economy as a whole. In a deflationary environment, consumers and businesses delay spending and investment, expecting prices to continue to fall. This can lead to decreased demand, lower production, and ultimately, higher unemployment rates. The German economy is one to watch as it has historically been a one of the strongest in Europe. when Germany's economy is weak, it can have a negative impact on the rest of Europe. A slowdown in German manufacturing can lead to reduced demand for goods and services from other European countries, which can lead to lower economic growth and higher unemployment. Germany is also a major trading partner for many European countries, so any changes in Germany's trade policies or trade relations with other countries can have significant consequences for the rest of Europe. In addition, Germany plays a key role in the European Union (EU) and the Eurozone. As the largest economy in the Eurozone, Germany has a significant say in economic policy decisions that affect the entire region. Germany also provides significant financial support to other EU countries, particularly during times of economic crisis, so any changes in Germany's economic policies or priorities can have a ripple effect throughout the rest of Europe. It will be interesting to see how this develops as their economy could foreshadow what is next for the remainder of Europe. Lower Inflation: A Double-Edged Sword for the Global Economy The second indicator (or indicators) that we'll look at are inflation and employment data. The annual inflation rate for the US edged lower to 4.9% in April 2023, the lowest since April 2021, from 5% in March. [3] Food prices grew at a slower rate, and energy cost fell, namely gasoline and fuel oil. Shelter cost, which accounts for over 30% of the total CPI basket, slowed for the first time in two years. When you take out food and energy, the CPI rose 5.5% on the year and 0.4% on the month, in line with market forecasts. [4] Overall, the annual inflation rate in the US is expected to remain steady at 5% in April 2023, still much above the 2.1% average reported from 2000 to 2020. [5] Keep in mind the Federal Reserve has a dual mandate to promote price stability and maximum employment. The first role of the Fed is to keep inflation in check. They want to maintain stable prices and avoid both deflation (falling prices) and excessive inflation (rising prices). This is important because high inflation can erode the value of money, reduce purchasing power, and create economic uncertainty. The second role of the Fed is to promote maximum employment, which means achieving a level of unemployment that is consistent with full employment. This is important because high levels of unemployment can lead to reduced economic growth, lower consumer spending, and social problems. As you can see, there is still plenty of work to do when it comes to getting inflation back down to 2%, and the April employment information may support a Fed decision to keep raising interest rates. Total nonfarm payroll employment rose by 253,000 in April, and the unemployment rate changed little at 3.4%. [6] However, this month's report showed the change in total nonfarm payroll employment for February and March was revised down. With these revisions, employment in February and March combined is 149,000 lower than previously reported. [7] This is a sign that we're not adding jobs as fast as previously reported, which might mean that April's report could be revised down in the future. Also, the NFIB Small Business Optimism Index for April fell to it's lowest level since January of 2013, and reported that 49% of owners were expecting better business conditions over the next six months. [8] In other words, the majority of the small business owners surveyed believe that business conditions will get worse over the next six months. Considering the decline of demand that we're seeing in the economy, it would make sense that has business owners feel pressure financially that they'll have to resort to laying off workers. Banking crisis continues to cast a shadow on the economy Finally, a continued banking crisis points to the potential of a deflationary economy. This past week, PacWest stock plunged 23% after losing 9.5% of deposits. [9] We continue to see that people are concerned about the safety of their money being held with regional banks. This is concerning because regional banks are the biggest source of loans for small businesses. A small business is defined as a business with less than 500 employees. Using that designation, about half of the employed population in the US is employed by a small business. So let's connect the dots here. As regional banks continue to see their deposits decline, they will tighten their credit standards and be less willing to loan money. This will negatively impact small business loans and potentially place a heightened financial burden on the small businesses that are dependent on loans to keep operating. This will ultimately trickle down to the employees in the form of unemployment. Conclusion In conclusion, I think the economic indicators presented in this article support the beginning of a deflationary economy. It is important to note that a deflationary economy can have serious consequences for both individuals and businesses. Inflation can erode the value of savings and investments, but deflation can lead to a decrease in economic activity, which in turn can lead to job losses and reduced spending power. As consumers and business owners, it is crucial to pay attention to these economic indicators and adjust our strategies accordingly. For individuals, this may mean taking a more cautious approach to spending and investments, while for businesses, it may mean finding new ways to increase demand or streamline operations to reduce costs. Abundance is here to help you prosper regardless of what happens next in the economy. Our Directional Portfolios aim to build a portfolio that will adjust with the business cycle. If you'd like to learn more, you can call or text at 678.884.8841 or email us at connect@findabundance.com . The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Investment Services, LLC or Kestra Advisory Services, LLC. This is for general information only and is not intended to provide specific investment advice or recommendations for any individual. It is suggested that you consult your financial professional, attorney, or tax advisor with regard to your individual situation. Endnotes: HCOB Germany Manufacturing PMI, April 2023, https://www.markiteconomics.com/Public/Home/PressRelease/84c628d3c6e04e87a2660c3f940846a2 HCOB Germany Manufacturing PMI, April 2023, https://www.markiteconomics.com/Public/Home/PressRelease/84c628d3c6e04e87a2660c3f940846a2 Trading Economics, United States Inflation Rate, https://tradingeconomics.com/united-states/inflation-cpi Trading Economics, United States Inflation Rate, https://tradingeconomics.com/united-states/inflation-cpi Trading Economics, United States Inflation Rate Forecast, https://tradingeconomics.com/united-states/inflation-cpi/forecast U.S. Bureau of Labor Statistics, The Employment Situation - April 2023, https://www.bls.gov/news.release/pdf/empsit.pdf U.S. Bureau of Labor Statistics, The Employment Situation - April 2023, https://www.bls.gov/news.release/pdf/empsit.pdf National Federation of Independent Business, NFIB Small Business Optimism Index - April 2023, https://www.nfib.com/surveys/small-business-economic-trends/ Yahoo Finance, PacWest Stock Plummets 23% After Losing 9.5% of Deposits, https://finance.yahoo.com/news/pacwest-stock-plummets-23-losing-001937377.html